Compare Tickers

Enter two financial asset tickers (e.g., T-MSFT/T-GOOGL). You can search tickers and copy them into a basket using the ticker selector.

Want to create plots with your own data series or price to sales plots?

Popular Tickers (Free Tier)

Trading Notes & Guide

General Notes

Currency Consistency: Ensure tickers are in the same currency to avoid exchange rate noise affecting the ratio.

See the currency on the Ticker Selector Page.

ETF Consistency: When plotting the ratio between two ETF's, always check that both are either distributing or accumulating. If this is not the case dividends can effect the results significantly!

Beta Correlation: Ensure the beta (calculated from montly periodic returns) is significant. Otherwise, you may be trading noise, and there will be no reliable reversal to the mean.

Recommendation: Always check the seasonality plot of the ticker you intend to swing trade; ensure the historical seasonality isn't moving against your position.

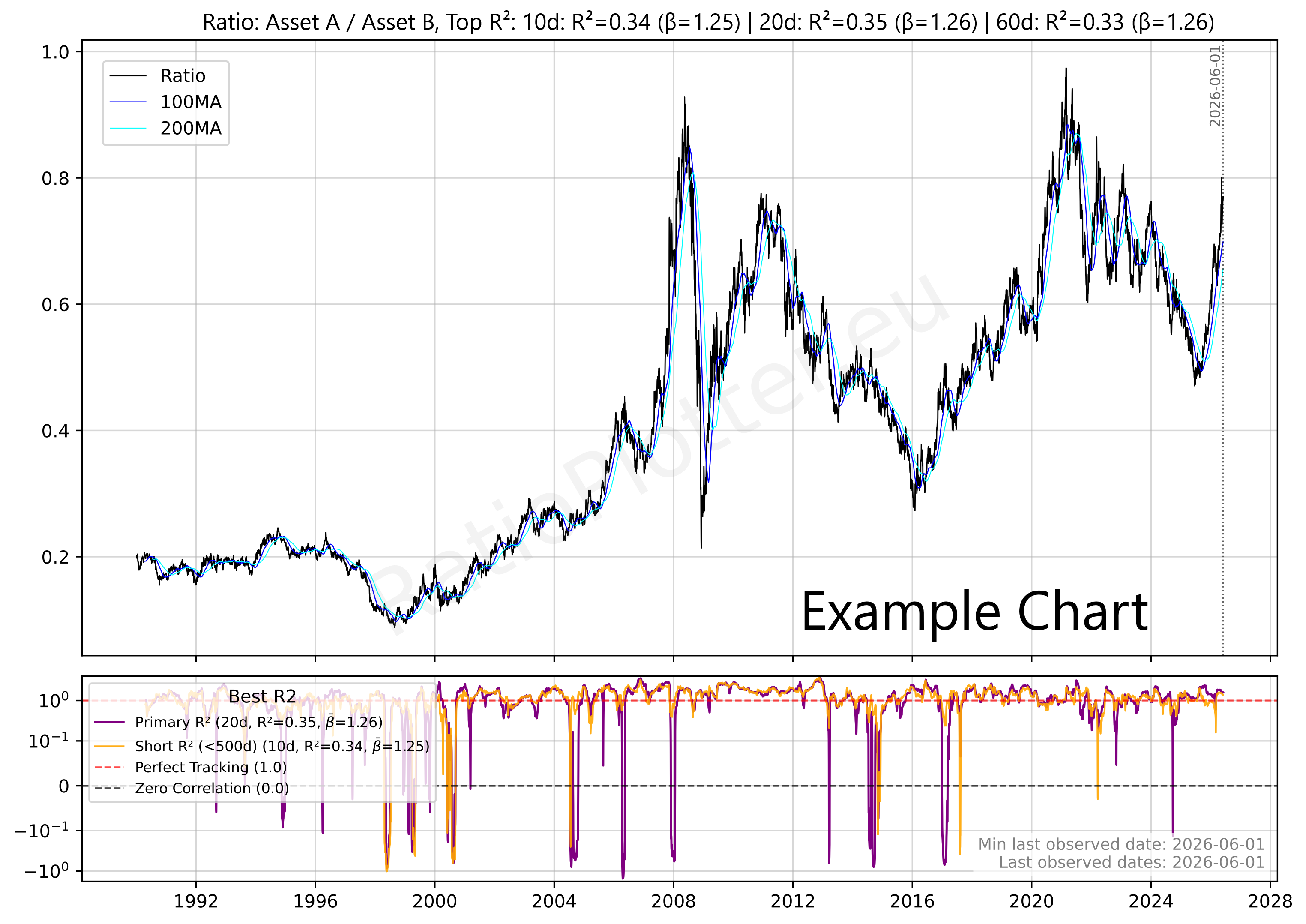

R2 and Beta Analysis Summary for Ratio Trading

To ensure a Ratio trade is based on structural correlation rather than random price movement, the R2 and Beta must BOTH be significant.

A low R2 indicates that Asset A and Asset B are "decoupled," meaning any apparent pattern in the Ratio is likely statistical noise with no mathematical pressure to return to the mean. Conversely, a high R2 confirms the assets are "tethered," making mean-reversion strategies reliable.

Besides the R2 we also need to make sure the Beta is healthy. The Beta between two assets indicates how much the numerator moves relative to the denominator. To use the Beta you can use this simple formula: Expected Numerator performance ≈ Denominator performance × Beta value.

A static Beta may mask recent shifts in relative volatility. To ensure your position sizing remains accurate, compare the overall Beta with the rolling Beta windows in the bottom dashboard pane. Monitoring these short-term fluctuations helps distinguish between normal market noise and a fundamental shift in how aggressively one asset moves compared to the other.

Statistical Warning: The R2 Validity Test

The following table defines the boundaries between random noise and actionable correlation based R2 values:

EXTREME CAUTION.

The assets are practically decoupled. No statistical reason for the Ratio to return to the mean.

Assets with a R2 value in this range can be used for diversifying portfolios.

CAUTION.

Significant risk of "drift" where the Ratio diverges permanently from historical averages.

Assets with an R2 value in this range provide little value for both diversification and mean reversion trading.

OPTIMAL.

Assets are tethered. High probability of mean reversion when the Ratio stretches.

Assets with an R2 value in this range are ideal for mean reversion trading.

Statistical Warning: The Beta Validity Test

The following table defines the boundaries between Inverse Ratio, Low volatility and high volatility asset pairs.

ATTENTION.

The assets move in opposite directions. A Beta of -1.0 indicates equal volatility but inverse movement. Assets in this range are primarily used for hedging strategies rather than standard Ratio trading.

EXTREME CAUTION.

The numerator asset is significantly less volatile than the denominator. The ratio will move slowly unless position sizing is adjusted.

Assets with Betas in this range can be used for diversifying portfolios.

OPTIMAL.

Both assets exhibit similar volatility profiles, meaning neither will easily overpower the other during price swings. This balance makes the pair optimal for standard 1:1 ratio trading, allowing for predictable mean reversion without the need for complex position sizing adjustments.

CAUTION.

The numerator is highly volatile relative to the denominator. While the assets may be correlated, this severe imbalance requires careful position sizing to prevent the numerator from overpowering the trade.

*Note: RatioPlotter.eu uses periodic returns (relative changes) to ensure the Beta and R2 reflect the structural relationship regardless of the absolute currency price of the assets.

Ticker Data Usage and Sourcing

Ticker Data Sources

SEA() Ticker function

RAT() Ticker function

LAG() Ticker function

MATH- Tickers

CURVE_FROM_VECTOR()

CURVE_FROM_VECTOR([198.27, 211.92, 245.12, 281.72, 318.27], '2026-06-30', 'last', '1y', 'linear', 'forward_fill')

The first argument is the time ordered list of data points, separated by commas. The second argument ('2026-06-30') is the one data anchor we need to plot these values over time.

The third argument ('last') tells the system to apply the anchor date to the last value, another value for this parameter is 'first'.

The '1y' tells the values fall on the exact same date on each year (or closest if leap year).

The '1y' could also be '1q' or '1m' for quarter or month. The same considerations made for year apply.

The 'linear' parameter tells the system how to interpolate the values for days in between the value data points given, another possible value here is 'forward_fill'.

The 'forward_fill' last parameter is about the extrapolation, its possible values are: 'none', 'forward_fill', 'linear'.

Default Ticker Column Projections & Adjustments

Plotting Dividends Reinvested at Your Portfolio Return Rate

This is a function available only for users with the advanced subscription. The first argument is the Ticker simulated, the second is your portfolio CAGR rate (in this case 0.25 = 25% yoy). We apply the daily equivalent rate though. The third argument is the initial investment in the currency of the stock ticker. The last argument is the start date. For a full example see our article on dividend reinvestment simulation.